It's a good idea to sit down and make a budget before you start looking for a vehicle. When it comes time to buy, knowing how much money you can afford to spend each month on a car loan will help you make the right option.

In addition to insurance and the total cost of ownership, your interest rate influences your monthly loan payment. Your credit score has a significant influence on interest rates. A good credit score usually results in a low-interest rate, but a bad credit score can result in a higher interest rate.

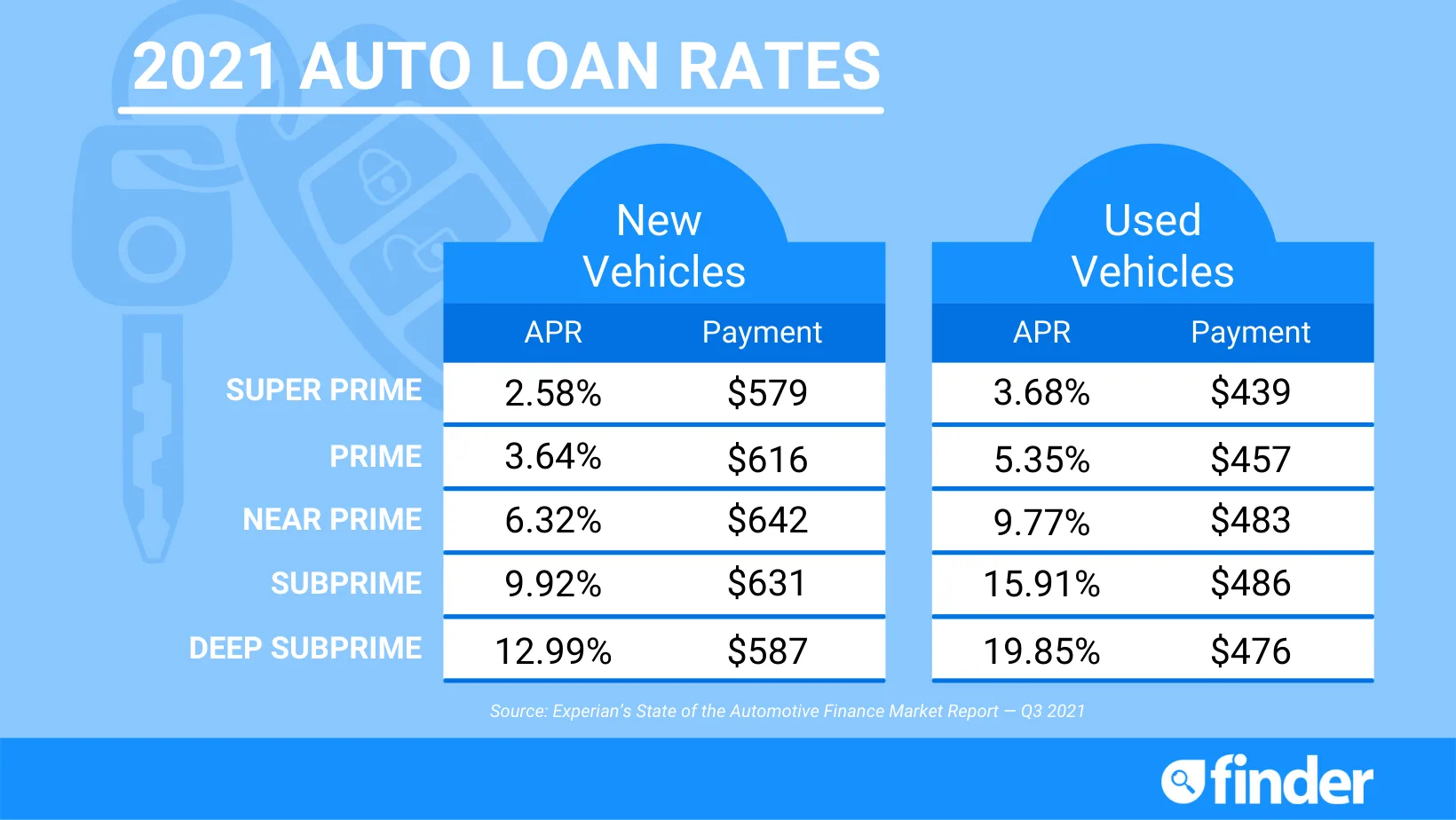

Furthermore, the real question is how to get a good interest rate. Full credit means you should expect a cheaper interest rate when financing a used car. An excellent approach to getting a low-interest rate is using debt responsibly, which gives you a higher credit score. If you have exceptional or good credit, you should be able to get a cheaper interest rate on an auto loan.

Reference: https://www.finder.com/car-loan-interest-rates

Extended Loan

Lenders frequently offer lengthier loan terms to new purchasers when purchasing a new car. However, the extended loan period will almost probably be factored into the interest rate. A longer loan usually means a higher interest rate and overall cost.

If you choose a secured personal loan, your car will serve as security or collateral if you cannot repay the lender. Cars depreciate quickly. Therefore lenders will account for this during the length of the loan. The lender will take a risk if you cannot repay your loan and your vehicle has depreciated or malfunctioned. After some time has gone, they may raise the interest rate.

Credit Score

Before applying for a car loan, experts recommend knowing your credit score. A lender values your credit score since it allows them to examine your debt payback history. Lenders will view you as a greater risk borrower if you have a lot of debt and expenses, resulting in a higher interest rate. You stand a better chance of getting a reduced interest rate if you have a good credit score.

Down Payment

The down payment is a percentage of the car's purchase price. Usually, 20% is paid in advance. Experts advise saving for a longer length of time to acquire a larger down payment on your loan.

Debit To Income Ratio

Your debit to-income ratio is figured by dividing your recurrent monthly debt payments (loans, credit card debt, and mortgage payments) by your recurring monthly income (investment dividends, salary, bonuses, etc.) Lenders want to look at this percentage since it shows how likely you are to repay your new loan.

For example, if you have a large gap between your monthly debt and income, it will be more problematic for you to get a loan. Even if you get one, your interest payments will be greater to compensate for the lender's increased risk. It's also worth noting that having debt can be preferable to having no obligation, as lenders will be unwilling to lend to someone who can't demonstrate a track record of payments.

At Canada Prime Autos, we are dedicated to assisting you in driving an automobile that you adore. We are here to help you comprehend vehicle interest rates and the elements that may influence the rate you qualify. We believe there is a car and financing solution that is specifically tailored to your needs. Learn more about auto finance below, or apply for an auto loan online to see what you might be eligible for. Please get in touch with a knowledgeable sales staff member, if need be.